The 182 days period can be consucative period or not. The deadline for filing income tax in Malaysia also varies according to what type of form you are filing.

Taxon Nov 12 Income Tax Summaries Kareen Received The Following Income From Her Employment In Studocu

Rental income in Malaysia is taxed on a progressive tax rate from 0 to 30.

. Non-residents are taxed a flat rate based on their types of. Here is a list of perquisites and benefits-in-kind that you can exclude from your employment income. Residence status affects the amount of tax paid.

- RM10000 for every completed year of service with the same employer companies in the same group. Foreigners who qualify as tax-residents follow the same tax guidelines progressive tax rate and relief as Malaysians and are required to file income tax under Form B. Foreign income remitted into Malaysia is exempted from tax.

The calculation of individual threshold of non taxable income is taking into account after the deduction of annual gross income with eligible individual reliefs and tax rebates. Malaysia Non-Residents Income Tax Tables in 2020. The rental income commencement date starts on the first day the property is rented out whereas the actual rental income itself is assessed on a receipt basis.

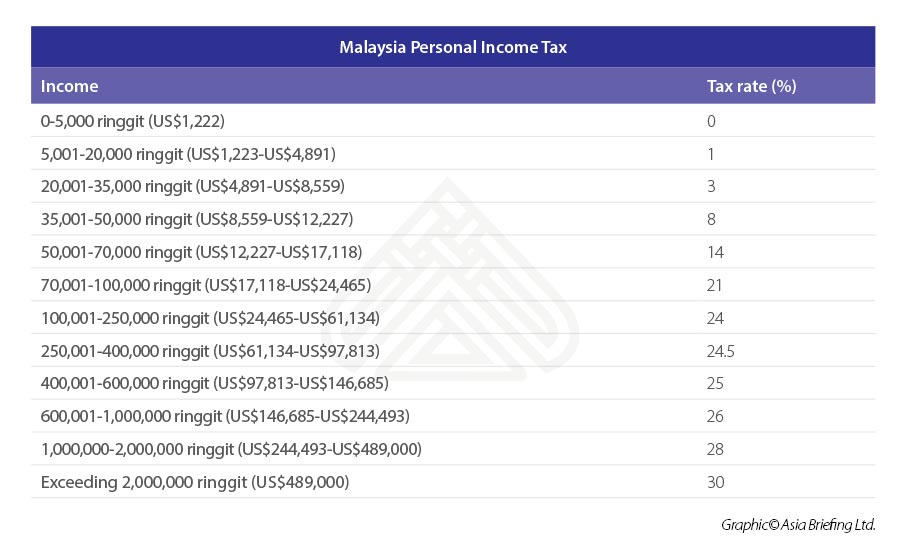

If the individual is Resident in regard to Malaysian Tax Law the individual. Income Tax Rates and Thresholds Annual Tax Rate. Non-resident stays in Malaysia for less than 182 days and is employed for at least 60 days in a calendar year.

Flat rate on all taxable income. If the subsidy is deemed taxable the employers are subjected to tax. Malaysia Non-Residents Income Tax Tables in 2022.

For both resident and non-resident companies corporate income tax CIT is imposed on income accruing in or derived from Malaysia. An Individual will be considered Non-Resident for Income Tax purpose if the individual is physically present in Malaysia for less than 182 days during the calendar year regardless of the citizenship or nationality. Such income will be treated equally vis-à-vis income accruing in or derived from Malaysia and taxable under Section 3 of the ITA.

Individuals who earn an annual employment income of more than RM34000 and has a Monthly tax Deduction MTD is eligible to be taxed. If the amount exceeds RM6000 further deductions can be made in respect of amount spent for official duties. Below are the income tax rates applicable to non-residents provided by the The Inland.

Compensation for loss of employment and payments for restrictive covenants. The source of employment income is the. Non-resident taxpayers ie.

Income derived in Malaysia by a non-resident public entertainer is subject to a final withholding tax at a rate of 15. Up to a limit of MYR6000 per year travel allowance petrol cards fuel allowance or toll payments for travelling in the exercise of employment are exempt from tax. A qualified person defined who is a knowledge worker residing in Iskandar Malaysia is taxed at the rate of 15 on income from an employment with a designated company engaged in a qualified activity in that specified.

Malaysia has implementing territorial tax system. Income Exempt from Tax. The current CIT rates are provided in the following table.

A resident status is someone stayed in Malaysia for more than 182 days about 6 months in a calendar year while a non-resident status did not. Flat rate on all taxable income. You are considered a non-resident under Malaysian tax law if you stay less than 182 days in Malaysia in a year regardless of your citizenship or nationality.

With paid-up capital of 25 million Malaysian ringgit MYR or less and gross income from business of not more than MYR 50 million. Parking allowances or fees. Between Rs 5 lakhs and Rs 10 lakhs.

5 of your taxable income. Non-resident individual is taxed at a different tax rate on income earnedreceived from Malaysia. The company has to pay 17 per cent tax for taxable income of less than RM500000.

Rs 12500 20 of income above Rs 5 lakhs. Resident individuals are taxed according to the tax rate and eligible for tax reliefs in accordance with section 45A - section 49 of the ITA 1967. Tax Exemption Limit per year Petrol travel toll allowances.

Current accounting standards state that the subsidy shall be treated as other income which means under normal circumstances this subsidy is taxable. Increased to RM20000 for individuals who ceased employment during the period from 1 January 2020 to 31 December 2021. While non-resident individuals are taxed at a flat rate of 30 and are not eligible to enjoy any reliefs.

Individuals corporates and others will continue to be exempted from income tax under Paragraph 28 Schedule 6 of the Malaysian Income Tax Act. A non-resident individual is taxed at a flat rate of 30 on total taxable income. The tax exemption would allow individual taxpayers to remit their income back to Malaysia tax-free and encourage them to continue to do so.

For further information consult the dedicated page on the official website of the Inland Revenue Board of Malaysia. Income tax in Malaysia is territorial in scope and based on the principle source regardless of the tax residency of the individual in Malaysia. Both residents and non-residents are taxed on income accruing in or derived from Malaysia.

Effectively income tax will be imposed on resident persons in Malaysia on income derived from foreign sources and received in Malaysia with effect from 1 January 2022. In summary the tax treatments for income of a. Income Tax Rates and Thresholds Annual Tax Rate.

Income Tax For Foreigners Residents and Non-Residents Image. Please be informed of Malaysia taxation on rental income for foreigners charged by Malaysia Inland Revenue differs by your status of either resident or non-resident in Malaysia. Nikkei AsiaYukinori Okamura.

Any source of income derived from outside Malaysia and received in Malaysia is tax exempted. As a result the employers are not. Contract payments to non-resident contractors are subject to a total withholding tax of 13 10 for tax payable by the non-resident contractor and 3 for tax payable by the contractors employees.

For the BE form resident individuals who do not carry on business the deadline falls on either 30 April 2022 manual filing or 15 May 2022. Residents and non-residents in Malaysia are taxed on employment income accruing in or derived from Malaysia.

Income Tax Relief Items For 2020 R Malaysianpf

Individual Income Tax In Malaysia For Expats Gpa

Malaysian Tax Issues For Expats Activpayroll

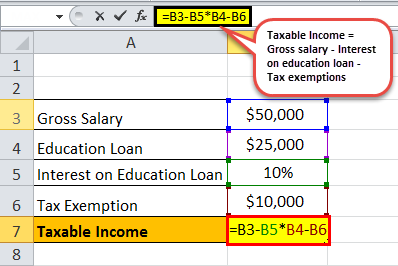

Taxable Income Formula Examples How To Calculate Taxable Income

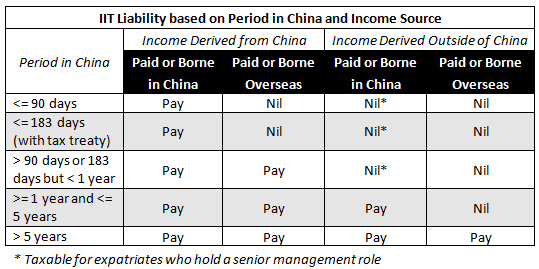

China Expat Tax Filing And Declarations For 2012 Income China Briefing News

Taxable Income Formula Calculator Examples With Excel Template

Taxable Income Formula Calculator Examples With Excel Template

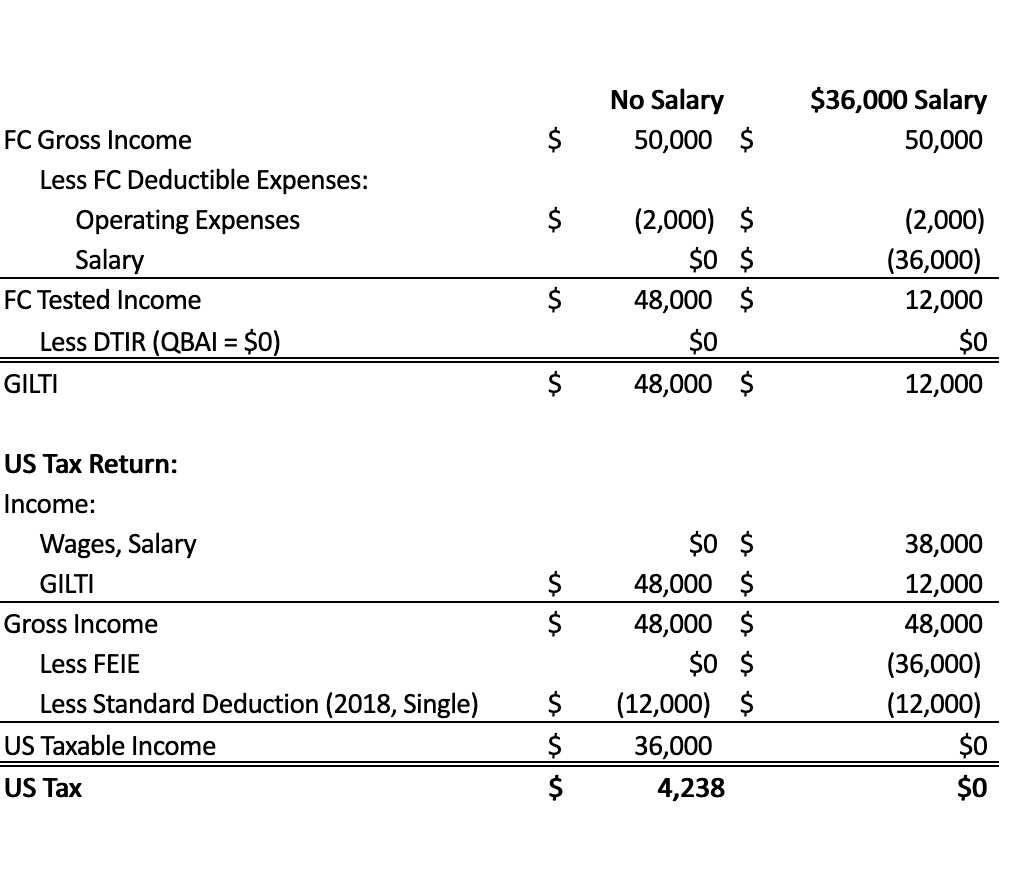

Getting To Know Gilti A Guide For American Expat Entrepreneurs

How To Calculate Foreigner S Income Tax In China China Admissions

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

Taxable Income Formula Examples How To Calculate Taxable Income

Calculating Individual Income Tax On Annual Bonus In China Updates Dezan Shira Associates

Solved Please Note That This Is Based On Philippine Tax System Course Hero

Taxable Income Formula Examples How To Calculate Taxable Income

Individual Income Tax In Malaysia For Expatriates

Updated Guide On Donations And Gifts Tax Deductions

Pdf Tax Simplicity And Small Business In Malaysia Past Developments And The Future Semantic Scholar

Guide To Tax Clearance In Malaysia For Expatriates And Locals Toughnickel

How Is Foreign Sourced Income Taxed Thannees Articles

- kuah hitam nasi kandar

- shopee express van driver

- kad pengenalan malaysia hijau

- tan sri zaman khan

- kalendar islam 2018 jakim

- undefined

- non taxable income malaysia

- aktiviti untuk kanak-kanak taska

- bulan sabit dan bintang bendera malaysia

- tema baju raya 2019

- department of labour malaysia

- batu pahat to kuala lumpur

- pkd kuala terengganu

- cara ganti nama coc gratis

- bilik sewa tawau

- sistem e-rpi

- kes air hitam 2016 berita

- resepi kek kukus coklat

- conditioner yang bagus untuk rambut kering

- kombinasi warna cat kelabu luar rumah